This article aims to provide a high-level analysis of the offshore wind market in Italy, both in terms of its potential development and its regulatory framework, to facilitate market participants considering entry into, or continued engagement with, that market. Further, the contributors set out some key considerations and issues for such market participants to think about in connection with their investments in the Italian offshore wind market.

Contributors

1 Italian GOVERNMENT TARGETS – PNIEC and PNRR – Road to 2030

In December 2019, various Italian ministries announced the Integrated National Energy and Climate Plan (“PNIEC”). The PNIEC establishes a suite of goals for Italy’s energy transition. To achieve these goals the Italian government has announced the National Recovery and Resilience Plan (“PNRR”) to raise €23.78bn to help meet national decarbonisation goals.

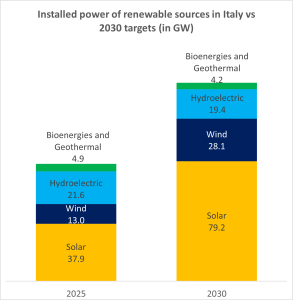

The targets in the latest version of the PNIEC, updated in June 2024¹, forecast an increase in installed renewable power capacity in Italy from the current 66 GW² to 131 GW by 2030.

This provides the backdrop to a general perception of rapid growth in the renewables sector in Italy. Wind energy is projected to make up a large portion of this growth. The current installed wind capacity in Italy is 13 GW³; but is forecast to rise to 28.1 GW by 2030.

Source: Terna https://dati.terna.it/en/generation#installed-renewables and PNIEC

2 Italian Offshore Wind Market – Background

Optimism for the Italian offshore wind sector is driven by (amongst other things):

- Potential for Growth: studies by Turin’s Politecnico University estimate Italy’s potential for floating offshore wind power at 207.3 GW. This makes Italy, according to the Global Wind Energy Council, the third largest market in the world in terms of potential for developing floating offshore wind projects. Indeed, the current portfolio under development in Italy is approx. 84.3 GW.

- Geography: Italy has 8,300km of coastline and a valuable barycentric position in the Mediterranean. This means Italy has the coastline, and location as a logistical hub, to be an important jurisdiction for offshore wind development in Europe. Of course, the development of the offshore wind industry in the Mediterranean area will play an important role in the parallel development of the Italian offshore wind market.

- Infrastructure: Italy has an advanced network of ports and fifty-seven harbours. According to a recent study conducted by The European House – Ambrosetti, offshore wind technology could facilitate the rapid build out of five key sectors in Italy that are already strong and will be required for the development of a substantial offshore wind industry. These are: construction materials; metal products; advanced mechanics; shipbuilding; and electrical equipment. According to this study, Italy is the European leader for the manufacture of metal products (€99.8bn) and ships and boats (€6.6bn). It is also second in the EU after Germany for advanced mechanical engineering (€40.7bn), electrical equipment (€26.3bn) and building materials (€82.2n). Considering the depth and specific characteristics of the Mediterranean Sea, steel and concrete production for the platforms will be crucial, as well as the use of specific support vessels in order to install, operate and maintain the floating wind turbines.

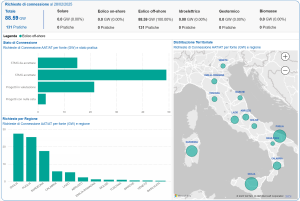

This explains the excitement in the wider market about the Italian offshore wind sector. Although there is currently only one operational offshore wind farm in Italy (the 30 MW Taranto offshore wind farm); as of February 2025, 88.59 GW of offshore wind project connection requests had been made to grid operator Terna and seven of these projects are at an advanced stage of development (i.e the environmental impact assessment procedure). Overall, there are 131 offshore wind farm projects planned for Italy.

Key market participants include both domestic investors (e.g. Renexia and GreenIt) and international investors (e.g. Copenhagen Infrastructure Partners, BayWa r.e. and Bluefloat). A number of such developers have made significant commitments to the Italian wind energy sector and estimate its potential growth far above the targets of the Italian government.

These proposed projects tend to be in the southern Adriatic, the Ionian, off the south coast of Sardinia and off the coast of Emilia-Romagna (see chart below):

Source: Terna https://www.terna.it/en/electric-system/efficient-territorial-planning/econnextion

Legislative framework for offshore wind projects in Italy

All this development/potential for Italian offshore wind begs the question; what is the legislative framework for building an offshore wind farm in Italy?

Regulation of the Italian coastline

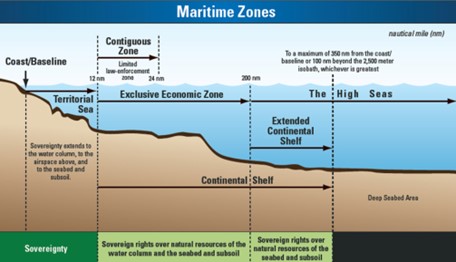

Italy, in common with the states with a coastline adjacent to or facing Italy (except Libya), is a party to the 1982 United Nations Convention on the Law of the Sea. Per the map below, this provides that states have (i) full sovereignty in their territorial seas; (ii) certain enforcement rights in a “Contiguous Zone”; (iii) certain specified sovereign rights in an “Exclusive Economic Zone”; and that (iv) the high seas and international seabed area fall outside of national jurisdiction.

In June 2021, the Italian Parliament authorised the establishment of an “Exclusive Economic Zone” (the “EEZ”) beyond its territorial sea.

Maritime areas under UNCLOS. Source: NOAA Office of Ocean Exploration and Research

This provides the framework for zones where Italian offshore wind farms can be built.

Based on the available information, the offshore wind farms under development are not only located in Italian territorial waters, but also beyond the 12 nautical miles.

Key authorisation

There is no public pre-qualification procedure or tenders in general for operators of offshore wind farms in Italy in relation to obtaining authorisations and / or grid connection.

There are three main authorisations that are required:

- Maritime Concession – this is granted by the Ministry of Infrastructure and Transport and essentially provides land rights for the occupation and use of the maritime and land state property, including areas used for the cable route and interconnection works;

- Single Authorisation – this is granted by the Ministry of Environment and Energy Security in agreement with the Ministry of Infrastructure and Transport and in consultation with the Ministry of Agriculture Food Sovereignty and Forestry, through a complex procedure in which all relevant entities and authorities participate. Such procedure is to be completed within 120 days of the first meeting of the Steering Committee; and

- Environmental Impact Assessment Decree – this is granted by the Ministry of Environment and Energy Security in agreement with the Ministry of Culture. It confirms the offshore wind farm impact on the environment.

These main authorisations will be issued as part of a single authorisation procedure that will involve an investigation by relevant persons into the activities of the offshore wind farm.

Grid connection

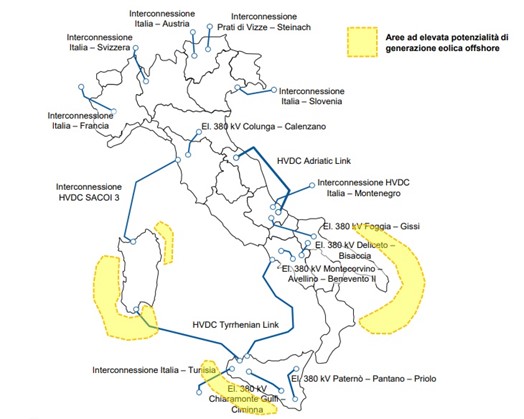

The operator of the national transmission grid (Terna S.p.A.) and the operators of the local distribution grids (Terna S.p.A. and / or E-Distribuzione S.p.A.) must ensure renewable energy plants are connected. This is regulated by the modalities and contractual conditions for the supply of the interconnection service issued by the relevant grid operator and the resolutions issued by the Italian Regulatory Authority for Energy Grid and Environment. In evaluating the geographical areas of key interest for future grid connections, in 2021 Terna S.p.A. circulated a map of the areas with high potential for offshore wind power production (see below (i) South Adriatic/Ionian (ii) the Mediterranean and (iii) southern Tyrrhenian):

Source: https://www.terna.it/

In a report published in June 2024, the non-profit association WindEurope, after analysing the status of grid connections in several European countries including Italy, highlighted grid connection delays and current backlogs. According to the report, saturated electricity grids are fast becoming the biggest obstacle to an accelerated renewable energy uptake across Europe. It is worth noting that at the end of 2023, Terna approved the 2024-2028 industrial plan⁴, which provides for the highest level of investments in its history of €16.5bn over five years.

Incentive regime

The new Italian decree for government incentives for renewable energy projects (i.e. fonti energetiche rinnovabili “FER 2”) (first announced in 2018) came into force on 13 August 2024.

A summary of the key terms that will apply under FER 2 to floating offshore wind farms and fixed bottom offshore wind farms located at least 12 nautical miles from the coast is set out below:

- Competitive tender process: access to these incentives is limited to new constructions. The incentive is granted through online participation in a competitive public procedure announced by the Gestore dei Servizi Energetici (the “GSE”) for the period 2024 – 2028. In this period, a power capacity threshold of 3.8GW is available for offshore wind farms;

- Dates: there will be at least three procedures over the five-year period of FER 2. Their dates are to be confirmed;

- Tariffs: The basic tariffs for competitive procedures in 2024 for offshore wind farms is set at €185/MWh. This value is valid for 25 years. In subsequent years, this will be reduced annually by 3%. Project owners must offer at least a 2% percentage reduction on the basic tariff;

- Contract for difference mechanism: payments start from the project commercial operation date. The incentive works by calculating the difference between the tariff due and the market price of the energy and (i) where this difference is positive, the GSE will pay the incentive by applying a premium tariff to the production injected into the grid and (ii) where this difference is negative, the GSE adjusts or requests the corresponding amounts from the producer;

- Requirements for access: project owners need all of the following to be eligible for the incentive: (i) to hold the Single Authorisation or alternatively, a favourable environmental impact assessment decision for the project (as described above); (ii) to hold a definitively accepted grid connection estimate; (iii) be compliant with the minimum environmental and performance requirements set out in FER 2; and (iv) be a floating offshore wind farm or a fixed bottom offshore wind farm located at least 12 nautical miles from the coast;

- Rankings: to be drawn up at the end of each allocation round; and

- Time to reach operation: projects must reach commercial operation within 60 months from the publication of the allocation rounds, net of any “downtime” in the construction of the plant and related works arising from force majeure. There are tariff reductions for each month that a project is delayed beyond this timeframe.

Key issues and considerations for Offshore Wind Investment in Italy

We set out below certain key issues for investors to consider when entering the Italian offshore wind market:

- Local stakeholders: an investor will need to have a good level of in-person support in Italy to interact with local stakeholders to progress any offshore wind project;

- Permitting timelines: consent can be one of the most time-consuming stages of offshore wind development. There may be challenges and delays with obtaining consent for early large projects in Italy whilst mitigating potential environmental and social impacts;

- Incentive regime: the FER 2 indicates a power capacity threshold of 3,800 MW available for offshore wind plants in the period 2024-2028. This is considerably below the current Italian offshore projects under development and the Italian government’s energy targets for energy produced from renewable energy sources. In addition, due consideration shall be given to the aggressive requirement that projects reach commercial operation within 60 months of the publication of the allocation rounds;

- Technical challenges to offshore wind development in Italy: To date, installations in Italy have included only one near-offshore plant. Italy faces technical challenges moving to large floating offshore projects. Specific complexity derives from: meteorological and geological constraints, as well as water depth and the need of new technology, all directly impacting the installation of offshore turbines in the Mediterranean;

- Supply chain development: whilst Italy has an extensive pipeline of offshore wind projects, the national supply chain is still developing compared to other markets. It is expected that Italy will work to increase local capabilities to capture the economic benefits available from offshore wind development. Italy is currently in its ramp-up phase with potential re-conversion / opening of new business units of existing local companies to provide the services required by the offshore wind industry;⁵ and

- Impact of Chinese supply chain:it is notable that the only operational wind farm in Italy uses Ming Yang turbines for its 30 MW project. This was the first use by a European offshore wind farm of turbines delivered by a Chinese OEM. The success of this process led, in August 2024, to Renexia (the developer of the offshore wind farm), Minister Adolfo Urso from the Ministry of Enterprises and Made in Italy and Ming Yang signing a memorandum of understanding for a Ming Yang/Renexia joint venture to build wind turbines in an Italian factory and supply 18.8 MW turbines for Renexia’s ambitious 2.8 GW Med Wind floating project. So, this is a space for those in the sector to keep an eye on.

[1] European Commission (2024) – Italy, Final updated national energy and climate plans (NECP) (submitted in 2024) – Link

[2] Source: www.gse.it

[3] Source: Terna https://www.terna.it/it/sistema-elettrico/dispacciamento/fonti-rinnovabili and PNIEC.

[4] Source: https://www.terna.it/en/media/press-releases/detail/2024-2028-industrial-plan-results-31-december-2023

[5] We note that in April 2024, the Ministry of Environment and Energy Security published a notice seeking expressions of interest from a least two ports in the south of Italy to be used for the construction of infrastructure suitable for the development of investments in the shipbuilding sector for the production, assembly and launching of floating platforms and electrical infrastructure to build offshore wind farms. This received strong interest from the applicable ports.