1) VIETNAMESE GOVERNMENT TARGETS

Renewables Growth

Vietnam’s national power development master plan is issued every ten years by the government.¹ This master plan sets out the key principles and objectives for national power development and the high-level plan for achieving them. The national power development master plan for 2021 to 2030 (with a vision to 2050) was approved by the Prime Minister of Vietnam on 15 May 2023 under Decision No. 500/QD-TTg (“8th Power Development Plan” or “PDP8”).

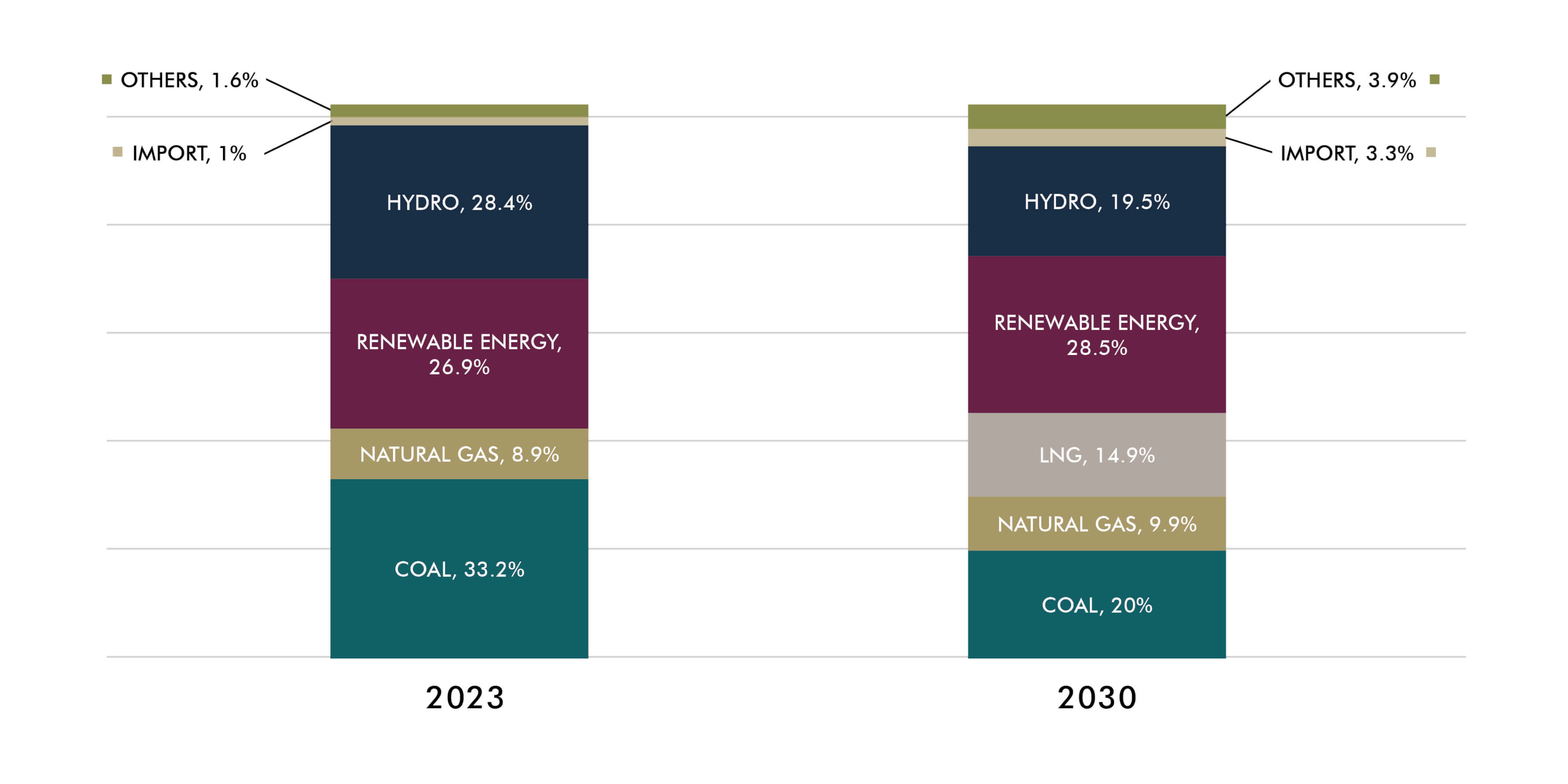

Under the PDP8, the total installed capacity of the power system is planned to increase from 80 GW in 2023 to 150 GW in 2030. The capacity of renewable sources (including wind, solar, and biomass) is expected to double from 21 GW (accounting for around 26.9% of the system) in 2023 to 42 GW (accounting for around 28.5% of the system) in 2030.

Under the PDP8, the total installed capacity of the power system is planned to increase from 80 GW in 2023 to 150 GW in 2030. The capacity of renewable sources (including wind, solar, and biomass) is expected to double from 21 GW (accounting for around 26.9% of the system) in 2023 to 42 GW (accounting for around 28.5% of the system) in 2030.